NA panel defers bill on banks taking over mortgaged homes after 90-day default

A National Assembly panel has deferred a bill that would allow banks to proceed with the sale of mortgaged homes after a 90-day default notice period. Lawmakers raised concerns that the proposed foreclosure framework could give excessive powers to banks.

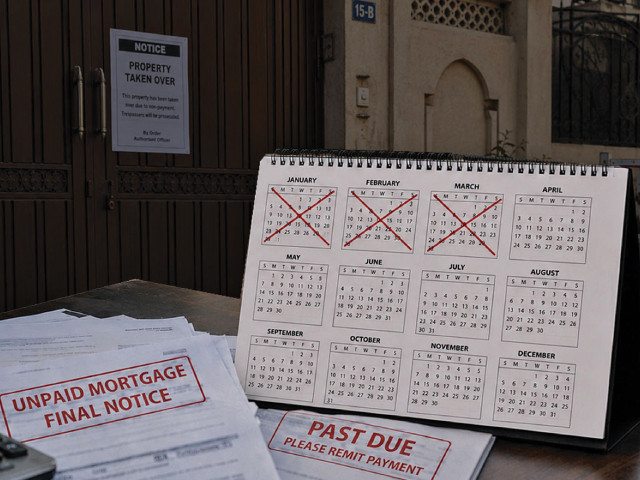

ISLAMABAD: The government has decided in principle to give commercial banks broader powers to take possession of mortgaged houses in cases of payment default after a cumulative notice period of 90 days, as part of efforts to encourage lending to the housing sector.

The proposed foreclosure legislation, which seeks to amend The Financial Institutions (Recovery of Finances) Ordinance, 2001, is currently under review by the National Assembly Standing Committee on Finance and Revenue. Under the draft, if a customer fails to pay mortgage dues, a financial institution may issue three notices of 30 days each demanding payment of the outstanding amount.

In case of default in payment by a customer after service of the final (third) notice, the financial institution may proceed with the sale of the housing unit, provided that all notices have been duly served upon the mortgagor, who has remained in default of payment of mortgage dues or any part thereof.

The standing committee met in Islamabad on Thursday under the chairmanship of former finance minister Syed Naveed Qamar and voiced strong reservations over what it saw as harsh provisions that appeared to favour banks over borrowers. In a written statement issued after the meeting, the committee said it had expressed concern over clauses that could potentially give banks excessive authority in the foreclosure process.

Committee members said that while a workable legal framework was needed to promote mortgage financing and protect lending institutions, sufficient legal safeguards and due process were also necessary to shield borrowers from arbitrary or unfair action.

After detailed discussion, the committee postponed consideration of the bill until its next meeting and directed the secretary of the Ministry of Housing and Works to circulate a revised draft among members for further review and input before finalisation.

Qamar said affordable housing finance should genuinely benefit deserving low-income families through transparent, accountable and inclusive arrangements. He also stressed the need for strong foreclosure and recovery laws to support Pakistan’s underdeveloped mortgage finance sector and improve the confidence of financial institutions in expanding long-term housing finance.

Briefing on Apna Ghar Programme

The federal secretaries of finance, housing and works, and law and justice also briefed the committee on the Prime Minister Apna Ghar Programme (PM-AGP), its implementation framework and proposed reforms linked to housing finance and foreclosure laws.

Housing Secretary Captain (retd) Mehmood Ahmad told the meeting that the PM-AGP was a subsidised housing finance initiative designed to help low and middle-income families buy homes while also promoting economic activity and reviving the construction sector.

According to the briefing, the scheme was approved in August 2025 and revised in March 2026. It offers financing of up to Rs10 million for first-time homeowners at a fixed markup rate of 5pc, repayable over 20 years with a 90:10 financing ratio.

As of April 30, 2026, the committee was told, 25,304 applications had been received. Of these, 8,990 applications worth Rs37.154bn had been approved, while Rs5.071bn had been disbursed to 1,845 beneficiaries.

The meeting was informed that Pakistan’s housing finance sector remained underdeveloped, with mortgage financing accounting for only 0.3 per cent of GDP and 0.56pc of total private sector credit. The government has set a target of financing 500,000 housing units over the next four years, requiring an estimated Rs3.2tr in financing.

Replying to a question, Finance Secretary Imdadullah Bosal said the government did not have fiscal space of Rs3.2tr, but because the initiative was a priority of the prime minister, funding would have to be arranged through various fiscal adjustments. He said subsidy schemes also needed review and added that the Public Sector Development Programme might have to be reduced further if required.

Proposed legal changes

The government side told the committee that changes in foreclosure and recovery laws were necessary to lower risks for banks, improve investor confidence and support sustainable growth in mortgage finance.

The committee observed that the housing finance sector required structural reforms, better foreclosure and recovery laws and a more supportive regulatory environment to encourage banks and financial institutions to expand mortgage lending. Members were also unanimous in expressing concern over the limited reach of housing finance for low-income and marginalised groups, especially in rural and underserved areas.

The panel also questioned whether banks and financial institutions had the institutional capacity and preparedness to meet the target of financing 500,000 housing units in four years, given the current state of the mortgage finance system.

It recommended that the government and the State Bank of Pakistan introduce simpler financing procedures, more flexible eligibility criteria and stronger subsidy support for low-income and informal-sector households to improve access and affordability.

The law secretary told the committee that the proposed amendments to The Financial Institutions (Recovery of Finance) Amendment Act, 2026 included several structural changes based on stakeholders’ feedback. These include the addition of a new Section 15A dealing specifically with housing finance instead of applying the provisions broadly to all mortgage deeds.

He said the revised draft extended the notice period in mortgage default cases, with the first three notices carrying 30 days each, making a total of 90 days before further proceedings. He added that a new proviso had also been inserted to allow financial institutions, at any stage before the sale of mortgaged property, to reschedule, restructure or settle outstanding mortgage liabilities.

According to the law secretary, the proposed changes were aimed at ensuring timely recovery, fair treatment of mortgagors and effective enforcement of secured interests, while maintaining efficiency and transparency in the recovery process.

Comments

No comments yet. Be the first to join the discussion!